Industry Trends: Market Analysis of Lubricants and Additives

Part.1

Lubricant market

Global lubricant market

In the 21st century, although the supply and demand of lubricating oil in the world have fluctuated, they have basically maintained stable growth. The overall global consumption of lubricating oil is facing difficulties in actual statistical work due to differences in sources and ranges. According to incomplete statistics, the global consumption of lubricating oil increased from 39.6 million tons to nearly 46.6 million tons from 2013 to 2018, with an average annual growth rate of 3.53%. In the demand for lubricating oil, automotive oil accounts for 54% and industrial oil accounts for 46%. The above statistics do not include marine oil. Currently, the global demand for marine lubricating oil is about 2.5 million tons/year, of which marine cylinder oil accounts for 50%, about 1.25 million tons/year, system oil accounts for 35%, about 875000 tons/year, and medium speed engine oil accounts for 15%, about 375000 tons/year. Asian shipping companies account for over half of the global demand for ship lubricants.

According to a 2014 research report, the global lubricant market sales in 2013 were $123.64 billion, and it is expected that sales revenue will reach $178.87 billion in 2020, with an average annual growth rate of 5.4%. From 2014 to 2020, the global lubricant market's shipment volume will continue to grow, reaching 49.1 million tons by 2020, with an average annual growth rate of 3.2%.

The annual per capita consumption of lubricating oil in the world is about 5 kilograms, but regional differences are very significant. The consumption in North America exceeded 18 kilograms in 2013. The per capita consumption in the Asia Pacific region is less than 4 kilograms, while in Africa it is only 2 kilograms. The per capita consumption in Western Europe is about 9 kilograms, in Eastern Europe and the Middle East it is close to 8 kilograms, and in Latin America it is just over 5 kilograms. As an engine of global economic growth, the Asia Pacific region will continue to maintain its dominant market position, with its global market share expected to increase from 41% in 2011 to 48% in 2020.

Chinese lubricant market

The combined consumption of the world's top 20 lubricant consuming countries accounts for 75% of global lubricant demand. In 2017, the apparent consumption of lubricating oil in China was 6.739 million tons, a year-on-year increase of 12.89%. Affected by macroeconomic factors, growth slowed down in 2018, but it remains one of the world's largest lubricant consuming countries. However, after excluding marine oil, the per capita consumption of lubricating oil is still less than 4 kilograms, indicating that there is still huge growth potential in the Chinese market. The United States ranks second, India is the third largest consumer country, followed by Russia, Japan, Brazil, Germany, South Korea, Mexico, and Iran.

There are many data on the consumption of lubricating oil in China in recent years in domestic public literature, but due to different statistical and calculation methods, there are significant differences in the data. For types of marine oil, rubber filling oil, white oil, etc., some statistics do not include them in the scope. In addition, the apparent consumption of lubricating oil in public data is only the sum of production and import/export differences, without taking into account inventory factors, and inventory has significant differences due to significant fluctuations in oil prices, which are the reasons for statistical data differences. The following figure shows the statistical analysis of China's apparent consumption of lubricating oil by research institutions from 2008 to 2017. With the continuous growth of China's automobile ownership and the gradual recovery of industrial enterprises, it is expected that the apparent consumption of lubricating oil in China will reach 6.87 million tons, 7.1 million tons, and 7.3 million tons respectively from 2018 to 2020.

Apparent Consumption of Lubricants in China from 2008 to 2017 (Unit: 10000 tons,%)

From the above table, it can be seen that the consumption of lubricating oil in China fluctuates greatly. The deviation caused by the statistical data sources is mainly due to the economic stimulus effect caused by increased investment from 2009 to 2012: the sharp increase in industrial oil quantity has led to a significant increase in China's lubricating oil production and sales, with lubricating oil consumption exceeding 8.5 million tons in 2012. However, the growth driven by investment is difficult to sustain, and the economy has since entered a "new normal", with a significant decrease in industrial lubricant consumption. At the same time, the rapid development of China's automotive industry, especially the passenger car market, has led to changes in the structure of domestic lubricating oil products: the proportion of industrial oil has decreased, and the demand for automotive lubricating oil (natural engine oil, gear oil, hydraulic oil, automatic transmission fluid, lubricating grease, etc.) is rapidly increasing. By 2016, the proportion of automotive internal combustion engine oil has accounted for more than 51% of the total lubricating oil.

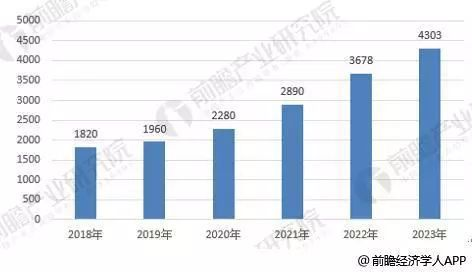

In 2016, China's annual automobile production and sales reached 28 million units, achieving double-digit growth for three consecutive years, continuing to become the world's largest automobile market and the world's largest consumer of lubricants. The demand for automotive lubricants in China has maintained a high growth rate of over 5% every year, and it is expected that by 2021, the internal combustion engine oil will exceed 5 million tons. The rapid growth of domestic demand for automotive oil and the trend towards high-end automotive oil will drive the automotive lubricant industry into a period of rapid development. According to published data, industry associations believe that as China's economic share in the world increases, the national consumption of lubricating oil will also approach or exceed the global per capita level. Although it is difficult to maintain the growth of industrial oil in the past, with the increasing cost awareness of major oil manufacturers, the growth space of domestic industrial oil is increasing. Therefore, the overall demand for lubricating oil will maintain stable growth, and it is expected that the Chinese lubricating oil market will exceed a market size of 430.3 billion yuan by 2023. The demand for lubricating oil will maintain an annual growth rate of nearly 3.5%.

Forecast of Demand for Automotive Lubricants in China from 2018 to 2023 (Unit: 100 million yuan)

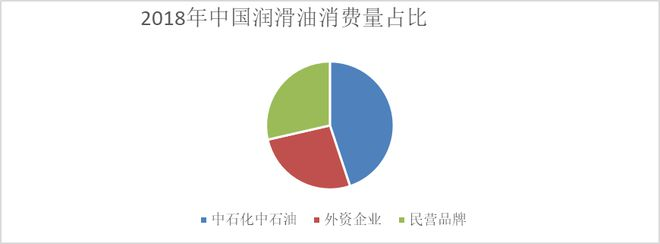

The proportion of Sinopec and PetroChina in lubricant production and suppliers has been decreasing year by year, from 44% in 2014 to 32% in 2018. The proportion of foreign brands has remained relatively stable at around 28%, while the proportion of private brands has increased rapidly, reaching 40%.

The proportion of lubricant consumption in China in 2018

Part.2

Lubricant additive market

Global additive market

Lubricating oil additives are compounds added to lubricating oil to give it various functional characteristics. Additives are mainly classified by function into types such as detergents, dispersants, antioxidants, anti-wear agents, extreme pressure additives, viscosity index improvers, etc. The additives sold in the market are generally a combination of the above single additives. The difference lies in the different components of the single additive and the different proportions of several single additives within the composite additive.

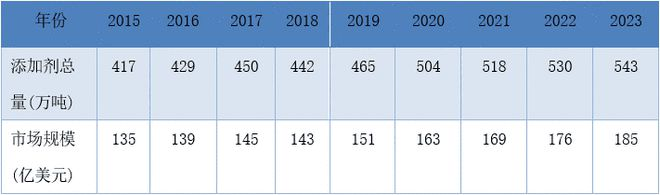

The total amount and market size of global additives from 2015 to 2018 are shown in the table below. It is expected that the market size will reach 18.5 billion US dollars by 2023, with an average annual growth rate of 3.4% from 2015 to 2023. Taking into account the rapid growth of emerging economies such as India and Brazil, as well as the impact of the Federal Reserve's suspension of balance sheet tightening on the global economy, the actual annual demand for lubricant additives has entered a new growth cycle, but the growth rate should be less than 4.6%.

Table 3 Global Lubricant Additive Market Size from 2015 to 2023

According to association statistics, the annual consumption of global lubricant additives also fluctuates over a certain period and range. From 2008 to 2013, the global market consumption of additives remained relatively stable, with a compound annual growth rate of 0.7%. However, China experienced a compound annual growth rate of over 5.7% during the same period.

According to global sector analysis, from 2011 to 2016, the global market consumption of lubricant additives remained stable, and the expected growth rate of consumption in the Asia Pacific region was faster than in other regions. During this period, the additive markets in Europe and North America experienced a decline, mainly due to the global economic recession from 2008 to 2010 and the 2011 European sovereign debt crisis. However, the rapid growth in consumption by emerging Asia Pacific countries represented by China and India during this period ensured the stability of global supply and demand.

According to the average compound annual growth rate of additives, it is expected that the global consumption of lubricant additives will increase to 4.4 million tons in 2018, with the proportion of additive consumption in the Asia Pacific region continuing to increase, and the share of shipments will reach 39.8% of the global total.

At present, the concentration of additives industry in foreign countries is relatively high, mainly led by the following four companies: Lubrizol, Infineum, Chevron Oronite, and Afton. In 2018, these four companies accounted for over 83% of the market share in lubricant composites. Among them, Lubrizol holds a leading position with a market share of 32.0%, followed closely by Runyinlian and Chevron, accounting for 23% and 20.0% respectively. In addition to the four major additive companies, there are also several smaller specialty additive companies that produce single agents, such as Chemtura, Basf, Vanderbilt, and Rohmax. Although these additive companies have small production volumes, they have global leading R&D capabilities in their respective fields and occupy a certain market share with their unique products.

In terms of the growth rate of demand for various lubricating oil additives globally, the top three annual growth rates from 2016 to 2018 were antioxidant 5.2%, dispersant 3.1%, and viscosity index improver 2.5%. The rapid growth of these three additives is due to their main application in passenger car engine lubricants and heavy-duty engine lubricants, which account for a large proportion of demand and are growing rapidly.

Chinese additive market

In the coming years, the Chinese market will be the fastest-growing terminal market for lubricant additives. The demand for lubricant additives in China was 750000 tons in 2013, and the total amount in 2018 was about 919000 tons, with an average annual growth rate of about 4.2%.

According to literature reports, the growth rate of additive demand in the global lubricant industry will exceed that of lubricants. Among them, antioxidants will have the fastest growth rate, with an annual growth rate of 4.9% by 2018; Next is dispersants, with an annual growth rate of 3%; The annual growth rate of viscosity index improvers is slightly higher than 2.5%; The annual growth rate of pour point depressants is about 2.4%.

In China, detergents, dispersants, and viscosity regulators are the most consumed types of lubricating oil additives.

The Demand and Changes of Lubricant Additives in China from 2013 to 2020

The expected growth rate of the consumption of lubricant additives in China is faster than that of other regions around the world. Based on the development trend of China's lubricant industry, industry associations conservatively estimate that the consumption of lubricant additives in China will increase to about 1.12 million tons by 2023, with an average annual growth rate of 3.5% from 2018 to 2023. The estimated consumption of lubricant additives in China by 2023 is shown in the table below.

Table 4 Prediction of lubricant additive usage in China from 2019 to 2023 Unit: 10000 tons